The US-Israeli conflict with Iran is dominating news headlines and markets around the world. The effective closure of the Strait of Hormuz, a primary artery for global energy, drove oil and gas prices significantly higher.

The supply shock extends to helium, essential for MRI scanners and used in semiconductor manufacturing. The Gulf States are major exporters of urea and sulphur. Disrupting the basic inputs to fertilisers feeds through to food prices.

In some ways it feels like déjà vu all over again: this time last year we were dealing with Trump’s trade war and now it’s all about Trump’s ‘Iran War’. So far, operation ‘Epic Fury’ hasn’t hit markets as hard as April 2025’s Liberation Day.

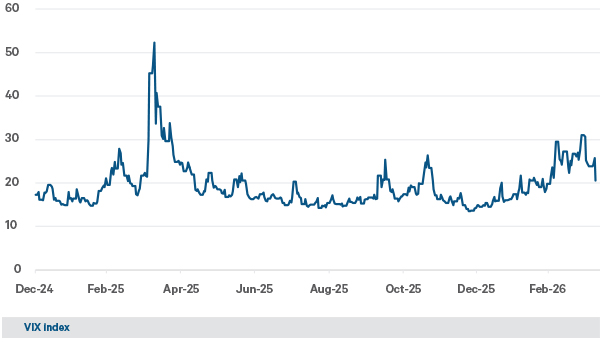

We can see this in the volatility index (VIX) for the S&P 500. Some people call it the ‘fear index’. Over the long term, the VIX has averaged 201 . In early January, the index was below 15, a sign that markets were calm. By the 9th of March, the Iran conflict had pushed the VIX to 35. Now, with a two-week ceasefire agreed, the index is back to 21. During the tariff shock last year, the VIX spiked over 50 and the S&P 500 briefly dropped into bear market territory, falling 20% from its high.

Since the US-Israeli operations began on the last weekend in February, global equities have declined 3% in euro terms. A stronger dollar, typical in risk off periods, has helped euro-based investors. In dollar terms, global equities are down 5%.

Figure 1: The volatility index (VIX) for the S&P 500

Source: Bloomberg, intraday 31st December 2024 to 8th April 2026.

1 A VIX reading of 20 indicates the market expects the S&P 500 to move approximately 20% on an annualised basis over the next 30 days, based on implied volatility from options prices. This equates to expected daily moves of approximately 1.25%.

People are often accused of ‘Trump Derangement Syndrome’. Maybe the market has developed Trump Immunity Syndrome? We know he can turn on a dime but a sustained end to the current hostilities and a full reopening of the Strait involves so many actors and interests, from Israel to the Iranian Regime, the Gulf States to the major Asian economies. More than 80% of energy exported through Hormuz is destined for Asia.

It’s difficult to predict what will happen in the Middle East and everyone has a view, from retired military generals to foreign policy specialists to energy economists. Normalisation of shipping will influence oil and gas prices, supply chains, inflation, and economic activity. Will the ceasefire hold or will the conflict resume? In the short term, market participants can speculate. Investing is about the long term.

Antebellum

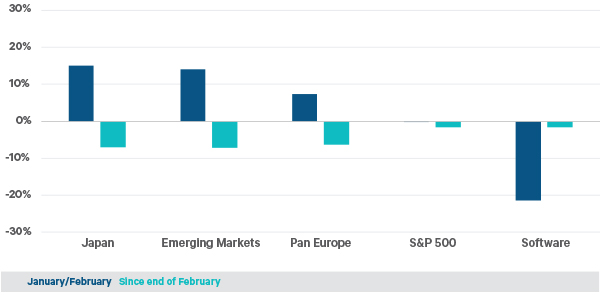

Before the Iran conflict began, stock markets were ticking along quite nicely. The more cyclical regions outperformed in January and February with equity indices in Japan and the Emerging Markets up in the mid-teens and Europe outperforming the US. The S&P 500 was flat in euro terms but overall, global equities were up almost 4%.

This was a market optimistic about global growth. Business surveys were pretty good. Earnings season went well. Monetary, fiscal and regulatory policy were supportive. Inflation wasn’t problematic. Economies were buoyed by capex tailwinds from spending on artificial intelligence (AI) and technology infrastructure, reshoring and reindustrialisation. Corporate balance sheets were in good shape.

Most of those positives still hold but with a big question mark over inflation and interest rates. Central bankers have told us they are waiting to see what happens.

Since the end of February, and in a reversal of the first two months of the year, the more cyclical regions have underperformed. The oil and gas importers in Europe and Asia, are more sensitive to the supply shock that the energy independent US.

Only one sector of the market has risen: Energy is up12%. Across the other sectors, the selling was fairly indiscriminate. Defensive industries, like healthcare, fell at least as much as the more cyclical sectors, like financials.

The SaaSpocalypse

In the first two months of the year, investors weren’t that worried about the US President. With mid-term elections set for November, he was expected to be relatively disciplined. He wasn’t the ‘Agent of chaos’ at the top of minds, instead the market was fixated on the ‘AI agents of chaos’. Concerns about disruption from developments in artificial intelligence hit software stocks hard. Software was the weakest industry group, declining 20% over January and February.

With the emergence of Agentic AI, the market is questioning the future earnings potential of the SaaS (Software-as-a-Service) companies. This includes the most established names in the industry like SAP and Salesforce, with valuations close to US$200bn each.

Smaller players have suffered more. Monday.com has a market value of less than US$3.5bn. In the global market of over 2,500 stocks across all the industrial sectors, it’s one of the weakest performers year-todate. Its share price has more than halved. Monday.com is a good example of where the fears about AI Agents are focused. As a cloud-based work operating system, the company provides project management software. It’s the type of task that an AI native tool, like Anthropic’s Claude CoWork, could do.

For Monday.com, technology disruption may be existential. For the bigger players, like SAP, disruption requires adaptation. Their core business is critical. Providing a system of record, deeply embedded into workflows, dealing with private company data and maintaining governance and audit trails.

AI is probabilistic. It’s trained to recognise patterns, and it can ‘hallucinate’. That doesn’t work when there is zero tolerance for error. Consider data protected by regulatory requirements or systems that need security permissioned access.

As advances in artificial intelligence increase the threat of competition, they will also create opportunities for productivity and growth.

Figure 2: Performance comparison - January and February versus end of February to date

Source: Bloomberg. Total returns in euro to 8th April 2026.

Life goes on

Despite the shifting landscape, merger and acquisition activity was strong in the first quarter, as companies executed plans to refine and strengthen their operations. It was the third consecutive US$1trn quarter for transactions. A record number of ‘megadeals’ were announced, with 22 deals valued over US$10bn.

The food and beverage industry was particularly busy. Cost conscious consumers have dented top line growth, so companies are seeking scale and synergies. Unilever agreed to sell its food division to spice maker McCormick, creating a group with a combined enterprise value of over US$60bn. Food distributor Sysco agreed to buy Jetro Restaurant Depot for US$29bn. Pernod Ricard confirmed discussions with rival Brown Forman.

Pricing it in

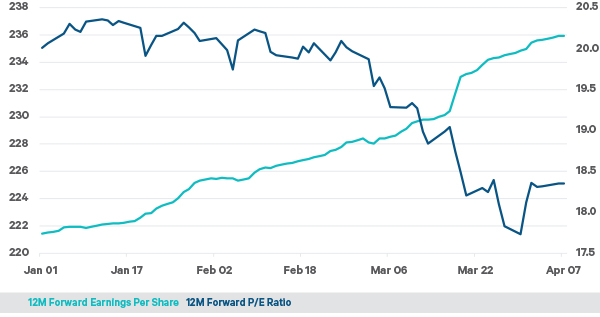

World equities are now unchanged since early February 2025, flat for over 14 months in euro terms. Collectively, valuations have derated to a little over 18 times 12 month forward earnings, having started the year above 20. Breaking it down by region, the S&P 500 is on 19.5 times earnings, down from 22. Europe is below 15 and Emerging Markets are at 11.5.

Overall, earnings estimates have been resilient with increases in some sectors, including energy, offsetting cuts elsewhere.

Revisions to near-term earnings forecasts will depend on a durable resolution to the conflict. However, markets are always looking ahead. With positive news, investors begin to price for recovery.

Figure 3: MSCI World Index price to earnings multiple and forecast earnings

Source: Bloomberg, 8th April 2026.

Crisis management

Over the last few years, companies have demonstrated a capacity to deal with various shocks. From COVID-19 in 2020, to Russia’s invasion of Ukraine in 2022, to the US tariffs last year.

If you were told at the end of 2019 that the world was heading into a major pandemic, followed by war in Europe, then an aggressively protectionist US, topped off with heightened conflict in the Middle East and an energy crunch, would you have invested in global equities? If you stayed in cash, you would have missed out on double-digit returns as a euro-based investor and as a dollar-based investor. It was a bumpy ride, but it was worth it.

Lessons from history

Double-digit performance through geopolitical shocks isn’t unusual. In early March, UBS released its ‘Investment Returns Yearbook’. The publication is compiled by Professor Paul Marsh and Dr. Mike Stanton of the London Business School and Professor Elroy Dimson of Cambridge University. They assessed the returns of the various asset classes going back to 1900.

Their research shows that bear markets during times of relative peace were the most difficult periods for stocks. The Wall Street Crash in 1929, the Dot-Com bust in 2000 and the Global Financial Crisis in 2008 were even worse periods for world equity returns than World War I or World War II.

Geopolitical events must be extreme to really matter. The rest is noise, although it may not feel like it at the time.