US equities sold off last week as the Middle East escalation impacted markets. Oil prices surged in response to potential supply disruption in the Strait of Hormuz. The dollar strengthened as investors moved towards safe havens. On the macro front, the ISM Services PMI came in at 56.1, its highest level since November 2022. Nonfarm payrolls data released on Friday showed that the US economy lost 92k jobs in February, with the unemployment rate ticking up to 4.4%.

Eurozone manufacturing strengthened, with the HCOB PMI rising to 50.8, its highest level in nearly four years. Inflation unexpectedly edged up to 1.9% in February, slightly above forecasts but still under the ECB’s 2% target. Unemployment fell to a record low of 6.1%. In the UK, construction activity contracted for the 14th consecutive month. Meanwhile, Brazil’s economy grew 0.1% in Q4 2025, as strong exports offset weak domestic demand.

Last week's highlights

|

- ISM Manufacturing & Services PMI (02/03 & 04/03) – Services PMI came in at 56.1, highest since Nov 2022. Manufacturing came in at 52.4.

- Initial Jobless Claims (05/03) – Unchanged from last week at 213k.

- US Nonfarm Payrolls (06/03) – Came in at -92k, big miss vs +55k forecast.

|

|

- HCOB Eurozone Manufacturing PMI (02/03) - Rose to 50.8 from 49.5, its strongest performance in nearly four years.

- Eurozone Inflation (03/03) - Unexpectedly rose to 1.9% in February, above 1.7% forecast but still below ECB target.

- Eurozone Unemployment Rate (04/03) – Fell to 6.1%, an all-time low.

|

|

- S&P UK Construction PMI (04/03) - Activity in UK construction sector contracted for the 14th month in a row.

|

|

- China Manufacturing PMI (04/03) - Fell to 49.0 in February, missing forecasts of 49.1.

- Brazil Q4 GDP (03/03) – Economy expanded by 0.1% in Q4 2025, as strong exports offset weakness in domestic demand.

|

Looking ahead to this week, markets will be hoping for an easing of tensions in the Middle East. In the US, investors will receive key inflation and labour market data, with CPI figures due on Wednesday and JOLTS job openings out on Friday. In Europe, German inflation data is also expected on Wednesday, followed by Eurozone industrial production on Friday. In the UK, Bank of England Governor Andrew Bailey is set to speak at the Financial Stability Board payments summit. Meanwhile in Asia, Japanese GDP and Chinese inflation figures will be released on Monday.

What's on the radar

|

- US CPI - February (11/03)

- US Core PCE Price Index (13/03)

- JOLTS Job Openings (13/03)

|

|

- German Inflation (11/03)

- Eurozone Industrial Production (13/03)

|

|

- UK BRC Retail Sales (10/03)

- Bank of England Governor Bailey speech (12/03)

|

|

- Japan Q4 GDP (09/03)

- China Inflation (09/03)

|

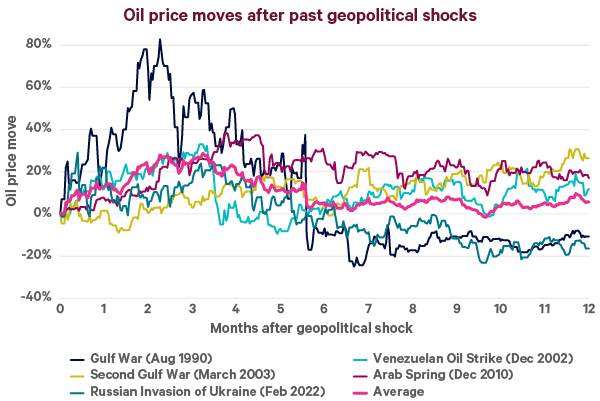

Chart of the moment - A jump at the pump, courtesy of Trump

Source: Bloomberg, UBS as of 06/03/2026. Brent crude oil price is used in the chart.

- Recent conflict in the Middle East has sparked an oil price rally, due to the risk of supply disruption through the Strait of Hormuz.

- Oil price spikes following geopolitical shocks are common. An analysis of past events shows that, on average, the oil rally fades within a few months.

- Fortunately, the global economy is now less sensitive to oil prices than it was previously. Only a major and prolonged disruption in oil supply would significantly impact global growth.