US equities recovered from a brief selloff after President Trump dropped the threat to impose 10% tariffs on European countries after announcing he reached a “framework of a future deal” on Greenland with NATO Secretary General Mark Rutte. Trump also stated that he “won’t use force” to take over Greenland. On the macro side, core PCE inflation in the US increased to 2.8% in November from October’s 2.7%. In the Eurozone, the HCOB Composite PMI came in at 51.5 - slightly below 51.9 forecast, but still in expansion territory. In the UK, inflation increased for the first time in five months to 3.4% in December, pushed higher by food costs and air fares. UK retail sales increased unexpectedly by 0.4% in December, boosted by online jewellery sales. In China, GDP growth hit the government’s target of 5.0% for 2025, as strong export growth offset weak consumption. The Bank of Japan left their key policy rate unchanged at 0.75% as expected, growth forecasts were revised up for 2026. The bank sees risks to growth & inflation as roughly balanced.

Last week's highlights

|

- US Core PCE Price Index (22/01) – Core PCE inflation in the US increased to 2.8% in November from October’s 2.7%.

- Michigan Consumer Sentiment (23/01) – Came in at 56.4 vs 54.0 forecast, reaching its highest level in five months.

|

|

- HCOB Eurozone Composite PMI (23/01) – Came in at 51.5, slightly below 51.9 forecast, but still in expansion territory.

|

|

- UK CPI December (21/01) - Increased for first time in five months to 3.4% in December, pushed higher by food costs and air fares.

- UK Retail Sales December (23/01) - UK retail sales increased unexpectedly by 0.4% in December, boosted by online jewellery sales.

|

|

- China GDP (19/01) - 2025 GDP growth hit the government’s target of 5.0%, as strong export growth offset weak consumption.

- Bank of Japan meeting (23/01) – Left key policy rate unchanged at 0.75% as expected, growth forecasts revised up for 2026. Board sees risks to growth & inflation roughly balanced.

|

Looking ahead to this week, the main event will be the Federal Reserve (Fed) meeting on Wednesday. Despite considerable pressure from the Trump Administration, no change in rates is expected. Earnings season is set to continue, with Microsoft, Meta, Tesla and Apple all due to report this week. Over in Europe, German GDP and inflation data will be released on Friday. The central banks of Brazil and Canada are also due to meet on Wednesday, with both expected to leave rates unchanged. Finally, investors in China will receive manufacturing data on Friday.

What's on the radar

|

- Federal Reserve Meeting (28/01)

- Producer Price Index (30/01)

|

|

- Germany Q4 GDP (30/01)

- Germany Inflation – January (30/01)

|

|

- UK Mortgage Approvals – December (30/01)

- UK Nationwide House Price Index (30/01)

|

|

- Bank of Canada Meeting (28/01)

- Brazil Central Bank Meeting (28/01)

- China Manufacturing PMI (30/01)

|

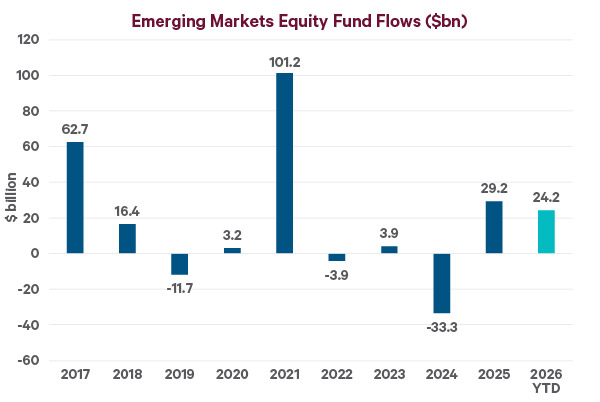

Chart of the moment - Tús maith leath na hoibre*

Source: EPFR Global, JP Morgan as of 23/01/2026, excludes on-shore funds. Values shown in billions of dollars. *'Tús maith leath na hoibre' is a popular Irish proverb meaning 'A good start is half the work'.

- Just a few weeks into 2026, emerging market (EM) equity fund flows have hit $24.2bn, close to the $29.2bn of total flows recorded in 2025.

- Investor interest in EM continues to strengthen, supported by cheap valuations and strong earnings forecasts. Policy uncertainty and elevated valuations in the US are forcing investors to diversify, positioning EM as an attractive alternative.

- 2025 was a breakout year for EM, returning 18% in euro terms versus 7% for global equities.

If you would like to stay up to date on the latest macro information, subscribe to this newsletter to receive it straight to your inbox every Monday.