US equities sold off last week as conflict in the Middle East continued to cast a long shadow over global markets. The Federal Reserve (Fed) left interest rates unchanged as expected, Fed officials increased their inflation outlook but still expect to cut interest rates once this year. The European Central Bank also held rates steady as expected, noting that the “war in the Middle East has made the outlook significantly more uncertain, creating upside risks for inflation and downside risks for economic growth”. Similarly, the Bank of England warned that rising energy prices could feed through to wages and require tighter monetary policy. Elsewhere, the Brazilian Central Bank cut rates by 25 bps, in line with forecast, to begin the cutting cycle. In Japan, the BoJ kept rates unchanged but noted that conflict in the Middle East will exert “upward pressure” on prices, as Japan gets about 95% of its energy imports from the Middle East.

Last week's highlights

|

- Producer Price Index (17/03) – Rose sharply in February, coming in at 0.7% vs 0.3% forecast.

- Federal Reserve Meeting (18/03) – Left rates unchanged as expected. Fed officials increased their inflation outlook but still expect to cut interest rates once this year.

|

|

- European Central Bank Meeting (19/03) – Held rates steady as expected, noting that “war in the Middle East has made the outlook significantly more uncertain, creating upside risks for inflation and downside risks for economic growth”.

- Swiss National Bank Meeting (19/03) - Left key policy rate at 0% as forecast.

|

|

- Bank of England Meeting (19/03) – Left rates unchanged as expected, stating that if the surge in energy prices is “larger or more protracted”, it could feed through to wages and require tighter monetary policy.

|

|

- Brazilian Central Bank Meeting (18/03) – Cut rates by 25 bps as expected after the effects of the Middle East conflict shifted consensus and market pricing from 50 bps to 25 bps.

- Bank of Japan Meeting (19/03) – Rates unchanged as expected. Officials noted that conflict in the Middle East will exert “upward pressure” on prices, as Japan gets about 95% of its energy imports from the Middle East.

|

Looking ahead to this week, the S&P Global Manufacturing & Services PMIs will be released in the US along with Michigan Consumer Sentiment figures. European investors will also receive PMI data with the HCOB Eurozone Manufacturing & Services PMIs set to be released. In the UK, both retail sales figures and inflation data are due out. Meanwhile, Australia will publish its inflation numbers, and Brazil will report its unemployment data.

What's on the radar

|

- S&P Global Manufacturing & Services PMIs (24/03)

- Michigan Consumer Sentiment (27/03)

|

|

- HCOB Eurozone Composite PMI (24/03)

|

|

- UK Inflation – February (25/03)

- UK Retail Sales (27/03)

|

|

- Australia Inflation (25/03)

- Brazil Unemployment Rate (27/03)

|

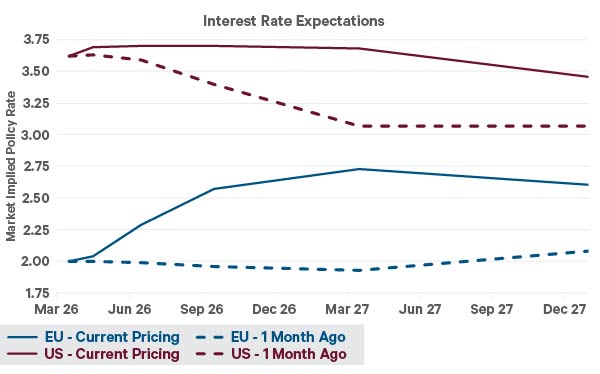

Chart of the moment - Best laid plans

Source: Bloomberg as of 20/03/2026

- Since the onset of conflict in the Middle East, markets have reset their expectations for interest rates moves this year, as energy prices have surged higher.

- Markets are now pricing almost 3 rate hikes from the European Central Bank (ECB) this year and are not expecting much movement from the Federal Reserve (Fed).

- Historically, central banks have tried to look through energy shocks, but they can only do so if inflation expectations remain anchored.

- The ECB are determined to avoid a repeat of 2022, when they underestimated the persistence of energy driven inflation, but they will need to be careful not to derail the economy in the process.