It's remarkable how many people can take a completely passive approach to their pension planning. Even busy, successful, high-net-worth individuals who are consciously building towards financial independence can sometimes have a blind spot when it comes to pension planning.

Others are simply content to let their pension pot ticking along in the background, more or less untended. There is a plan - somewhere - and the assumption is that all is well, the fund is growing, and there's nothing much to do except leave it alone and wait.

To an extent, this is understandable. We're all busy people. Time flies past, with the ever present to-do list showing no signs of diminishing. The idea of engaging with any major financial planning or decision making can seem daunting. It's far easier to put it off, deal with it some other time. And besides, what's to deal with? Isn't it taking care of itself?

Well, yes - and no! Your pension may be ticking along, but it is far too important to leave to its own devices. We're all living longer and fuller lives, with so much to look forward to in retirement - a little extra effort and attention now and you could be looking at an even brighter future, not only for yourself but for your loved ones.

Some simple steps and easy fixes can help you ensure your fund is in peak condition. And while there is no one-size-fits-all, there are certain universal hazards or traps that you can mitigate against.

1. Don't lose track of your pension pots

An easy enough thing to happen and may not seem like a huge deal in the short term, especially as you know 'roughly how much they are worth' and where to lay your hands on them - if you really need to. Longer term, however, having only a rough idea puts you at risk of losing control which could have negative consequences including potential loss of capital.

You may have heard that diversifying your pension investments and having multiple advisors is good practice, but the reality is that most people simply don't have time to properly manage multiple pension investments. It's important to take all your pension funds into account when reviewing your plans. You might even have built up several different funds into the same asset mix, giving you an unintended and risky concentration in one asset class.

2. How much of a pension do I need?

While the Irish State may indeed provide a pension, the maximum personal rate for a single person aged 66 or over is €289.30 per week, which equates to approximately €15,043.60 per year.

Don't underestimate how much money you will need in retirement. This will vary from individual to individual, and will depend on factors including long-term debt, perhaps helping a child or children to buy a house, or simply higher lifestyle spending requirements.

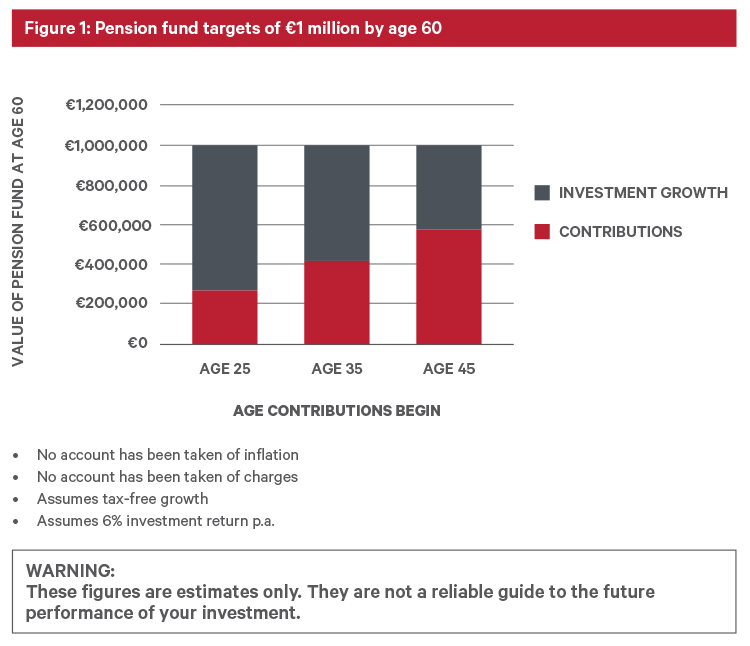

Whatever your target for retirement income, starting a pension as early as possible will pay off in the long run.

Figure 1 shows an example of three individuals targeting a pension fund of €1 million at age 60. The first individual started making contributions of €7,920 per annum at age 25. By age 60, their pension fund is made up of just 29% contributions and 71% growth on investment. Compare this with someone who started pension savings at age 45. To get to the same fund size at 60, they need to contribute €36,747 yearly. Their pension fund will comprise 59% contributions and 41% investment growth at retirement.

3. Find out what tax breaks you're entitled to

Another one of those 'rough' ideas that could be impacting your pension plan. You may be entitled to tax relief on pension contributions but do you know how much it's worth to you?

If you are a higher rate taxpayer, then subject to certain criteria and limits, for every €1 you contribute to a pension, the exchequer will give you back approx. €0.40. Even if you have never been self-employed or never had to file a tax return, you may have scope to make pension contributions that qualifies for tax relief in 2025.

Some employers will offer a company scheme that matches or even doubles employees' contributions. Your €1 contribution can translate into a €3 injection to your pension when you take account of your own contribution plus a €2 employer contribution. This is an obvious benefit to take advantage of.

4. Ensure you understand the fees involved

Not understanding, or worse, not paying attention to fees and charges, can have a significant impact on the future value of your pension pot(s). Most pension arrangements charge an annual management fee but it is vital that you also understand the costs associated with the specific fund(s) you choose. For example, commission, fund manager charges, bid/offer spreads and custody fees.

Your pension provider or advisor can provide you with a detailed breakdown of all costs associated with the operation and investment management of your investments - all you have to do is ask.

5. Make sure the advice you get is personal

Most pension arrangements offer a default investment strategy (DIS) for individuals who do not wish to make a specific investment choice. In practice, this typically means that as you approach retirement, your funds will move from higher risk assets into lower risk assets.

While this sounds like the proverbial safe bet, it's important to understand that a DIS is not risk-free - it can be volatile, and it will be affected by investment conditions and the wider economic environment in addition to the skill of the investment manager who is juggling these variables.

Remember you have little or no control over the transition of your funds from high risk to low risk, which means the prevailing economic and market conditions are not taken into account.

So what's the solution? Get the best advice of your life, for your life

If any - or all - of our 'hidden hazards' ring a bell with you, it's probably time for a thorough review of your retirement funding strategy. Those five universal pitfalls are a good starting point, but in order to really optimise your pension plan, getting expert advice is a good place to start.

At Davy, we understand that our clients are individuals, each with different financial goals. We don't do 'one-size-fits-all' pension plans because how much you need in retirement is different for everyone. Your retirement number is entirely personal to you. That's why we match you with highly-trained, specialist advisors who spend time getting a genuine understanding of your life and finding out what matters to you.