Naturally, a lot of us tend to avoid thinking about what would happen if we were no longer around. However, we all need to think about how assets can be protected and how loved ones will be looked after in that case. The starting point is to put a will in place, which deals with these issues, including who will have the legal responsibility to look after children, who will inherit specific assets, and how the transfer of assets should be structured. An important issue which overlays the transition of assets is how it can be done tax-efficiently.

Capital Acquisitions Tax (CAT) (which is a tax on gifts or inheritances) needs to be considered when assets pass under a will. It is payable by the recipient of the inheritance and the current rate is 33%. CAT operates on a cumulative basis. This means that all gifts or inheritances received since 5th December 1991 (a cut-off date set by legislation) which fall into the same class threshold are added together.

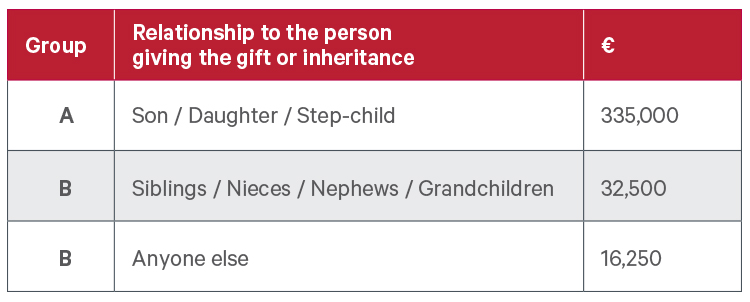

The thresholds are:

CAT will be payable on the value of inheritance or gifts which exceed the threshold.

Separately, any individual can receive an annual gift of €3,000 per annum tax-free from any number of people. The benefit of using the small gift exemption in this way means that the tax-free thresholds are not eroded. However, this exemption is not available against an inheritance.

One of the common problems which beneficiaries of estates have to address is how to fund CAT. Because of accelerated payment dates, the CAT may be payable within a very limited timeframe. In order to avoid interest and penalties, assets may have to be sold at inopportune times, or beneficiaries may have to source funds through bank lending if they do not have sufficient liquidity within their own asset portfolio to meet CAT obligations. A Section 72 policy can provide a solution to this problem. Unlike the proceeds of other life insurance policies, which are regarded as taxable assets and therefore subject to CAT at 33%, the proceeds of a Section 72 policy are exempt from CAT to the extent that they are used to pay the beneficiaries' CAT liabilities.

The importance of a will

Now that we have considered the potential CAT implications that beneficiaries may face on receiving an inheritance, it is also important for an individual to consider if they would like certain beneficiaries to get specific assets. Many people will have fixed ideas about who should inherit assets. While spouses have a legal entitlement (unless this is renounced) to receive a specific share under a will, children do not have a legal entitlement to receive any assets under their parents' will. In the absence of a will, an individual's estate passes using the rules outlined in the Succession Act. These rules could mean that the estate does not pass as the deceased would have wished. Therefore, a will is a very important document to have in place to ensure the deceased's estate can be administered in line with their wishes.

Once a will is in place, it is important that it is reviewed every 3 - 5 years or as circumstances change. Where an individual has minor children, or a child with a disability, consideration should be given to who the guardians and/or trustees will be. As minor children get older, there may be different issues to consider. Where there is property or assets located outside of Ireland, it is important that foreign advice is sought.

Careful consideration should be given to who the executors of the will should be and if they are prepared to act as executor. The role of an executor can be onerous and not everyone will be prepared to act. Furthermore, if the estate is complex, it can be advisable to have an executor who is familiar with financial matters to deal with these issues.

Finally, when preparing your will, you should consider if estate equalisation is important. If estate equalisation is your intention, it is advisable to keep a record of all gifts/loans etc. which have been made to children and allowance for any prior gifts etc. should be made in the will to ensure that the estate passes equally, if that is the intention.

Taking a proactive approach to succession planning is really important. It is essential to have a plan to deal with the transfer of assets to family and making sure that dependents are protected will give you a peace of mind. At Davy, we can help you make these important decisions.