In a market shaped by constant change, strategic asset allocation (SAA) provides the structure needed to build portfolios that can adapt and endure. It defines the balance between risk and return, shapes diversification, and ultimately guides each investor’s journey through different market cycles. The decision to allocate across asset classes over the long term is the single most important driver of portfolio returns, far more impactful than short-term tactical moves or the selection of individual active managers.

Our last major update to the SAA was in 2021. Since then, the investment landscape has changed dramatically. In 2022, both equities and bonds posted double-digit negative returns, a rare event that hadn’t occurred in over five decades. That year also marked a turning point in market dynamics, with inflation, interest rate volatility, and asset class correlations all shifting in ways that challenged traditional portfolio structures.

Considering these changes, we’ve been carefully reviewing the SAA across our core mandates; Cautious Growth, Moderate Growth, Long-Term Growth and Equity Growth. After thorough analysis, we now believe the time is right to make a change.

This update is not a reaction to short-term market noise, but a strategic response to a fundamentally different investment environment. Our goal is to ensure that each portfolio remains aligned with its long-term objectives, while continuing to manage risk effectively and capture opportunities in a more complex and interconnected world.

The case for change: A shifting investment landscape

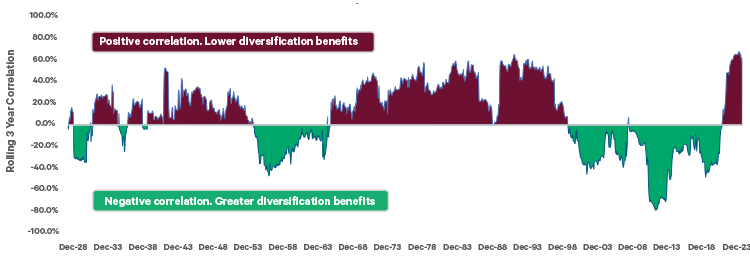

For much of the past thirty years, the negative correlation between equities and bonds has been a cornerstone of portfolio diversification. When equity markets declined, bonds typically rose in value, offering a natural hedge and helping to reduce overall portfolio volatility. This dynamic was largely supported by central banks’ ability to lower interest rates during periods of economic stress. These moves boosted bond prices and supported economic activity. As a result, the widely adopted ‘60/40 equity-bond portfolio’ became a go-to strategy: equities provided long-term growth, while bonds delivered stability and downside protection. This relationship held strong in a low-inflation environment, where central banks could act decisively without the risk of igniting inflation. However, that dynamic has reversed. Today, equities and bonds are more likely to move in the same direction, especially during periods of market stress. The turning point came in 2022 when both asset classes posted double-digit negative returns in the same calendar year, something that hadn’t occurred since 19721. This rare event was driven by a sharp surge in inflation and an aggressive response from central banks, who raised interest rates rapidly to contain price pressures. As a result, both equity and bond markets reacted negatively to the same macroeconomic shocks.

Figure 1: Correlation between US equities and bonds

Source : Ibbotson, Bloomberg and MSCI, based on rolling 3-year correlation.

This shift in correlation has persisted and is now reshaping how portfolios are constructed and managed. With bonds no longer providing the same level of diversification or downside protection, it has become essential to rethink traditional asset allocation strategies and explore new sources of resilience.

Crucially, this trend is not limited to one region. The positive correlation between stocks and bonds has become a global phenomenon. Across the U.S., eurozone, and Japan, inflationary pressures and synchronised policy responses have led to both asset classes moving in tandem. This has significantly eroded the diversification benefits that investors have long relied on to manage risk and smooth returns.

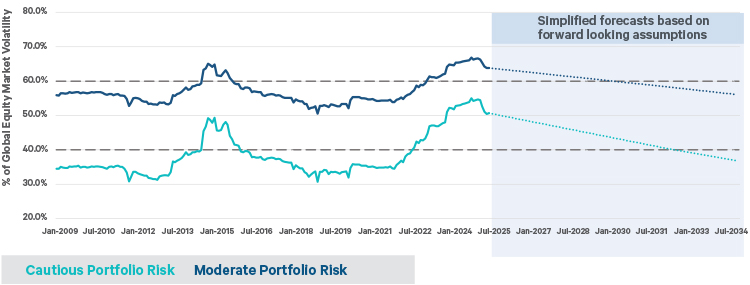

Since 2022, bond markets have also experienced a notable increase in volatility. Historically, bonds served as a stabilising force in diversified portfolios. But recent data shows that realised bond volatility has climbed to almost 6%, nearly double the 25-year average of 3.1%. This heightened risk from bonds further undermines the traditional role of bonds as a low-risk counterbalance to equities.

Figure 2: Volatility of Global Bonds and Global Equities

Source: Bloomberg and MSCI, based on rolling 3-year volatility

Risk based objectives on portfolios

We’ve designed our investment approach to meet the diverse needs of clients at different life stages and in varying financial circumstances. A key part of this process is ensuring that each client is invested in a portfolio that aligns with their individual risk tolerance.

Clients who are profiled as having a lower appetite for risk are guided toward portfolios that prioritise stability and capital preservation. Conversely, those with a higher tolerance for risk are matched with portfolios that offer greater growth potential, albeit with more risk.

The industry differs on methods to define portfolio risk; some use absolute volatility numbers and some rely on the percentage of equities in a portfolio to explain how risky a portfolio is. However, we believe this overlooks the risks that can arise from other asset classes. Instead, we assess total portfolio risk relative to global equity markets. This comparative framework provides a clearer picture of overall risk exposure, recognising that equities typically drive most of the portfolio risk over time.

Recent changes in market dynamics, particularly the shift in correlation between equities and bonds, have had a notable impact on portfolio behaviour. Traditionally, bonds helped reduce overall risk, especially in more cautious portfolios. But since 2022, bonds have become more volatile and now often move in the same direction as equities. This has caused our Cautious and Moderate Growth portfolios to operate outside their expected risk ranges.

While we allow for and expect some short-term deviations from our risk objectives, we do expect portfolios to remain within their designated bands over the long term. Many deviations can be short term in nature, however, it’s now clear that these recent trends are more persistent. Figure 3 plots the relative risk of the current Cautious and Moderate growth portfolios. Both portfolios are operating at higher than desired risk levels and are expected to stay elevated over the next few years.

Figure 3: Risk of representative Cautious and Moderate growth portfolios relative to global equities

Source : Davy, Bloomberg. Forward-looking assumptions are derived from JPM LTCMA 2025.

As a result, we believe it’s time to revise our long-term asset allocation strategy. By doing so, we aim to bring portfolio risk back in line with our intended ranges over the long term, ensuring that each client remains appropriately invested according to their risk profile.

Hunt for diversification

Our portfolios are carefully diversified across a broad range of asset classes, including equities, government and corporate bonds, gold, liquid alternative strategies, hedge funds, and property. This wide spread of investments is designed to reduce risk and improve the consistency of returns over time.

Within our government bond allocation, we maintain a long-term position in short duration inflation-linked bonds. These are bonds where both the principal and interest payments adjust with inflation, helping to preserve the real value of your investment. Because they have shorter maturities, typically under five years, they are less sensitive to interest rate changes, making them a more stable option in volatile markets. In today’s environment, where inflation remains a concern, these bonds play a valuable role in protecting purchasing power while managing interest rate risk.

One of the most important sources of diversification in the past has been the relationship between equities and bonds. However, as we’ve discussed earlier, this relationship has changed. Today, equities and bonds often move in the same direction, particularly during periods of market stress. This shift has reduced the effectiveness of bonds as a hedge. As a result, the diversification offered by other asset classes has a greater role to play in portfolios.

In our most recent strategic asset allocation update, we increased our exposure to gold. Gold has performed strongly in recent years and has contributed positively to portfolio returns. It has long been viewed as a store of value and a hedge against both inflation and geopolitical uncertainty. Importantly, gold tends to behave differently from both equities and bonds, making it a powerful diversifier in today’s market environment.

We’ve also increased the allocation to liquid alternatives in our portfolios. These are investment strategies designed to generate returns that are not closely tied to the performance of traditional stock and bond markets. They are available through liquid investment vehicles, meaning they can be traded daily or weekly—offering the accessibility of traditional investments with the sophistication of hedge fund-like strategies.

In a world where both stocks and bonds can decline at the same time, liquid alternatives provide a valuable source of diversification. These strategies can help smooth returns, reduce overall portfolio volatility, and offer the potential for positive performance regardless of market direction. Their flexibility is especially important in today’s complex environment, where inflation, interest rate changes, geopolitical tensions, and shifting economic growth all play a role in market behaviour.

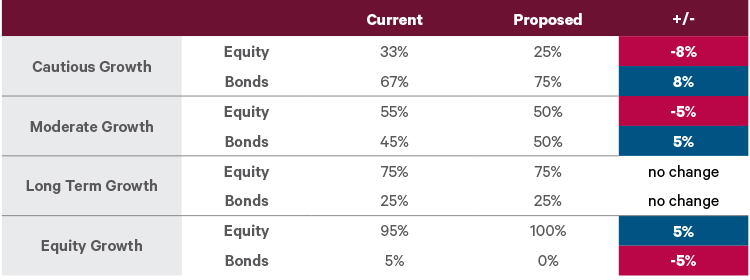

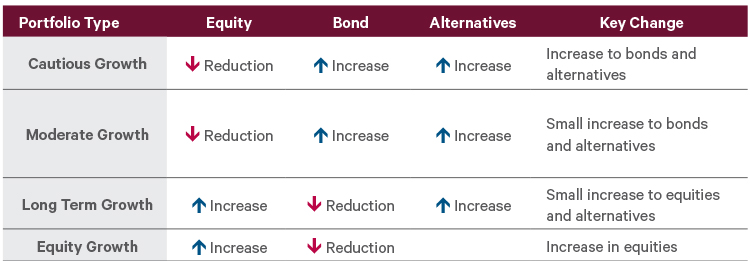

Figure 4: Valuation benchmarks: what’s changing?

Figure 5: Strategic asset allocation: What's changing?

Conclusion

The 2025 SAA update represents a thoughtful and data-driven response to a shifting investment landscape. By recalibrating equity exposures, enhancing diversification through alternatives, and aligning with forward-looking market assumptions, we aim to deliver robust, risk-adjusted returns for our clients.

These changes underscore the importance of dynamic portfolio management in an era of heightened uncertainty. Investors are encouraged to review these updates in consultation with their advisors to ensure alignment with their individual goals, risk tolerance, and financial circumstances.

1 The proxy of equity and bond indices varies in the industry. As we go further back in time, the issue becomes starker. You may see a different year being quoted as to when the last time a double-digit drawdown occurred in equities and bonds. The important thing here is that before 2022 it had not happened in a very very long time.