Speak to a member of our team

Request a call below

0 topics selected

30 October, 2020

Beyond words goes here

So far, 2020 has been a volatile year for markets. However, despite the dip into bear market territory, we have seen significant rebounds with the S&P 500 reaching record highs in August. This period of rising prices in most asset classes will have benefitted many clients in recent years. However, it has also brought about certain challenges, with one example being those impacted by the maximum tax efficient pension, known as the Standard Fund Threshold (‘SFT’).

In January 2014, the SFT was reduced from €2.3 million to €2.0 million. The combined value of an individual’s lifetime pension funds in excess of the SFT or (or Personal Fund Threshold for those with pension assets of sufficient value at the dates that thresholds have been reduced) is subject to punitive tax at retirement, prompting many people who are impacted to consider the most appropriate strategy for their pension assets. Many others whose pensions were valued below the €2.0 million threshold at the 1st January 2014 valuation date are now either above or close to the threshold. It is therefore timely to look at the most effective strategies that we have implemented for our clients who have been impacted.

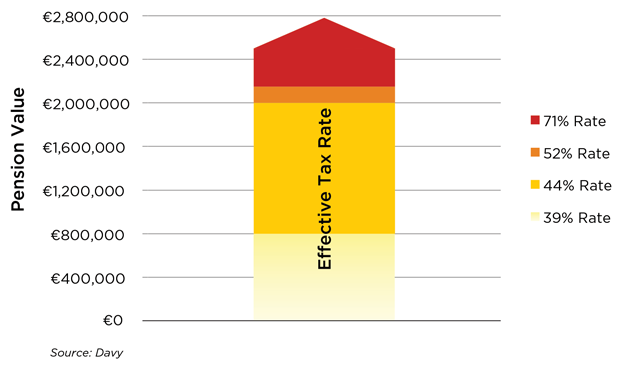

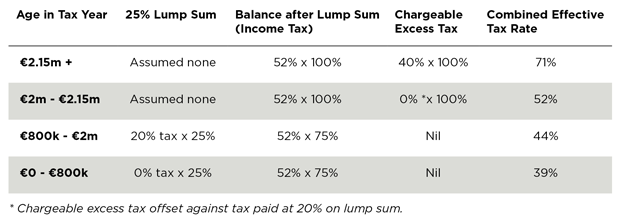

Pension contributions are one of the most tax efficient means of saving. However, a chargeable excess tax of 40% applies to pension assets over the SFT or PFT at retirement and this portion of the assets may be taxed again at higher income tax, USC and potentially PRSI when drawn as income of up to 52%. This leads to a combined effective rate of up to 71% on the excess amount (i.e. 100% – (40% * 52%)). It is not efficient to continue making pension contributions once assets have reached the threshold.

There is some respite from the chargeable excess tax applying to amounts over the threshold. Tax paid at a 20% rate on lifetime retirement lump sums can be used as a credit against chargeable excess tax. The maximum tax efficient retirement lump sum is set at 25% of the SFT and is currently €500,000. The first €200,000 of this lump sum is tax free, with the balance between €200,000 and €500,000 taxed at 20%.

Therefore, tax of €60,000 would be paid on a lump sum of €500,000 and this tax can be used as a credit against any chargeable excess tax that arises. This means that, in effect, there can be additional capacity for growth of up to €150,000 above the SFT or PFT before chargeable excess tax at 40% will need to be paid (€60,000/40% = €150,000).

Having assets valued above the SFT and the associated looming chargeable excess tax liability is likely to warrant a review of the investment strategy being adopted with pension assets. The cumulative tax rate of up to 71% on growth above the SFT means that the reward for taking risk is restricted, while there continues to be full exposure to loss. However, it is important to put this in context – even without a chargeable excess tax, growth above €2.0 million would effectively be taxed at marginal tax rates. It is also important to remember the benefit of the gross roll up treatment afforded to investment returns within the pension.

Figure 1. Effective tax rate on pension assuming 52% tax on income drawdowns

Source: Davy

*Chargeable excess tax offset against tax paid at 20% on lump sum.

Reducing the level of risk taken with the overall pension assets may be a sensible move. Concentrated investment exposures in particular may no longer be appropriate through a pension. The level of risk reduction will depend on a number of factors including time horizon, risk appetite and personal circumstances. For some, this may mean that the entire pension is converted to cash. For others, particularly those with a longer time horizon to accessing benefits and who don’t wish to forgo the potential for some upside, a lower risk diversified portfolio may be more appropriate.

Benefits are payable from age 60 in most pension schemes, but some people in occupational pension schemes may have access to their benefits from as early as age 50 where they are no longer in company service. For those impacted by the threshold, any further growth of pension assets will be taxed punitively when benefits are drawn, so it may make sense to access benefits at the earliest opportunity. This results in the value of the pension fund being crystallised for the purposes of the SFT: a lump sum is drawn and it may be possible to transfer the balance of the fund to an Approved Retirement Fund (ARF). The SFT does not apply to the value of the assets once transferred to an ARF and there is no obligation to pay taxable distributions from the account until the year in which the holder turns 61.

Some clients will be able to consolidate their accumulated pensions to a Personal Retirement Savings Account (‘PRSA’). One of the advantages of this pension structure is the ability to split larger pots into two or more smaller pension accounts which can be drawn at different times. This may be particularly beneficial for those who have total pension benefits in excess of the SFT or their PFT. It could be possible to split out their pension so that up to the maximum tax efficient amount is drawn at the earliest possible time with the excess above this amount deferred, potentially as late as age 75. Benefits of this strategy versus drawing retirement benefits from the full value of accumulated pensions include deferring the timing of the chargeable excess charge, the potential of improved death benefits and a reduced mandatory taxable withdrawal if choosing the ARF option.

As with most technical issues, the most appropriate strategy for each individual will depend on their own specific circumstances. The sooner the discussion starts, the sooner the most effective solution can be implemented.

Warning: The value of your investment may go down as well as up. If you invest in this product you may lose some or all of the money you invest.

Warning: The information in this article does not purport to be financial advice and does not take into account the investment objectives, knowledge and experience or financial situation of any particular person. You should seek advice in the context of your own personal circumstances prior to making any financial or investment decision from your own advisor. The tax information contained in this article is based on Davy’s current understanding of the tax legislation in Ireland and the Revenue interpretation thereof. It is provided by way of general guidance only and is neither exhaustive nor definitive and is subject to change without notice. It is not a substitute for professional advice. You should consult your tax advisor about the rules that apply in your individual circumstances. Davy is not responsible for the interpretation of this information and any submissions made by you or a third party on your behalf thereon.