Artificial Intelligence (AI) has emerged as a game-changer in the business world, revolutionising industries and transforming the way companies operate. From streamlining operations to enhancing customer experiences, AI has the potential to have profound effects on long-term company profitability. In turn, this could be translated into the price performance of a swathe of companies within global stock markets.

The adoption of advanced technologies in various industries, including automotive, healthcare, retail, finance, and manufacturing, is being driven by continuous research and innovation led by major technology companies. Artificial Intelligence has placed technology at the core of organisations, enabling its integration into almost every device and program, from self-driving cars to life-saving medical equipment.

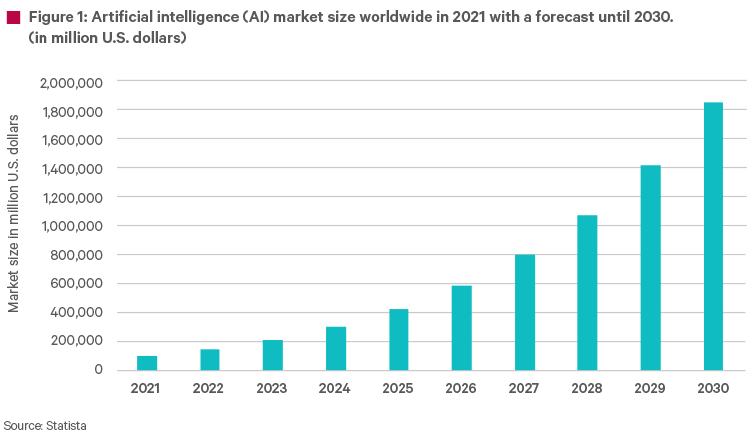

AI so far...

The worldwide market size for AI was valued at US$136.55 billion in 2022 and is expected to grow at a compound annual growth rate (CAGR) of 37.3% from 2023 to 2030. Consensus predictions are centred around robust growth in the AI market over the next decade.

The current market value is projected to increase approximately twentyfold by 2030, reaching nearly US$2 trillion in that year. This is based on the idea that the adoption of AI will span across various industries, encompassing supply chains, marketing, product development, research analysis, and more. Key trends in the AI landscape for the future include the advancement of chatbots, image generation AI, and business and mobile applications, all of which will contribute to enhancing AI capabilities.

AI in the market

As investors continue to ponder the potential impact of generative AI, one fundamental question arises: what implications could it have for the stock market? The recent performance of Nvidia serves as a notable example. The company, which is primarily focused on semiconductors, recently announced its projected sales of US$11 billion for the current quarter, surpassing the consensus estimate of US$7 billion by an impressive 53%. This surge in sales is attributed to the growing demand for its advanced chips driven by the advancements in AI technology. As a result, Nvidia has climbed to become the fifth-largest company in the S&P 500 Index.

This positive development in Nvidia's outlook has captivated investors, who are now analysing the extent to which generative AI will influence revenue growth and profitability across various industries. However, the potential impact of generative AI on corporate earnings remains uncertain in terms of magnitude and timing. In a report by Goldman Sachs Research, equity strategist Ryan Hammond explains that while generative AI could enhance corporate earnings, the specifics are still unclear.

Goldman Sachs Research analysts estimate that the adoption of AI, with its potential to boost productivity growth 1.5 percentage points annually over a decade, could result in a compound annual growth rate of 5.4% for earnings per share (EPS) in the S&P 500 over the next twenty years. This projection exceeds the 4.9% assumed by their current dividend discount model. Consequently, it suggests that the fair value of the S&P 500 could be 9% higher than its present value.

Dotcom 2.0?

This all sounds wonderful. However, if history is anything to go by, it is highly probably that A) the upside scenario trajectory is unlikely to be linear and B) that predicting things twenty years into the future is a near impossible thing to do.

In the late 1990s, technology companies experiencing rapid growth witnessed a collapse in their valuations when they failed to meet the lofty expectations of investors, despite their expanding sales.

Looking closer to home timewise, there are a couple of red flags beginning to appear as well. Narrow market leadership, whereby several large firms have been propping up the wider index performance for the year, is currently becoming prevalent. The majority of these firms are actively focusing on involvement within the AI space.

If we look at the S&P 500 price performance for 2023 so far, for example, we can clearly see where this becomes important. Excluding those firms that are heavily AI-driven, there is a notable difference in the year-to-date returns between this basket of stocks and the wider index. AI firms have had a surge in returns this year, which is not entirely harmonious to the broader market.

What this may be suggesting is that the wider index is potentially (more) cautiously assessing the current uncertainty around softening macro conditions as a result of overall tighter monetary policy from central banks. Simultaneously, investors may be anticipating the strength of growth estimates for AI firms is more than enough to handle any future economic weakness. The implication here is if this band of investors has been over-exuberant in their forecasting, there is a greater potential for these AI stock prices to fall, which in turn could then drag the index lower.

Beyond a pop...

While the advancements driven by AI hold great potential, airing caution against the risks associated with higher investor expectations, drawing parallels to the dot-com boom, is important.

That said, the situation does currently seem a little different. Long-term EPS growth expectations of the S&P Index are broadly in line with historical averages, indicating that investor confidence regarding AI adoption has not yet reached extreme levels. Additionally, stronger than expected recent economic data has helped underpin investor forecasts which may be perceived as a little ambitious.

However, certain individual stocks, particularly those benefitting the most from AI, are exhibiting valuations reminiscent of the dot-com era. As mentioned, if forecasted growth or profitability then becomes a little lacklustre in the short-term, these stocks may have gone a little too far too fast this year, leaving them vulnerable to pull-backs.