Financial markets by nature are inherently forward-looking, constantly trying to anticipate the next trend and predict how the future may differ from the present. The rapid emergence of artificial intelligence (AI) has intensified this debate, raising fundamental questions about which industries could be reshaped, disrupting incumbents and creating a new generation of market leaders.

One sector that has been firmly under the microscope of late is software, particularly software-as-a-service (SaaS). The SaaS industry has made its living over the past few decades selling a variety of software tools to business covering use cases in areas such as HR, Finance and Enterprise Resource Planning. SaaS companies typically provide their services on a subscription basis and generate revenue based on the number of users that have access to the software tools, an approach known as seat-based pricing. Since the initial launch of AI large language models or LLMs, such as OpenAI’s ChatGPT, there has been persistent concern about the implications for software business models.

Industry concerns sharpened in early January following the release of Anthropic’s Claude ‘Cowork’ application. Unlike a conventional chatbot, Cowork is positioned as an autonomous digital coworker, designed not just to assist, but to execute tasks independently. The impact on SaaS could be significant. If AI tools can increasingly perform these workflows end-to-end, investors are right to ask how value, pricing power, and customer demand may evolve. Beyond SaaS there are questions about the future of human labour in general, with these latest AI tools intensifying the debate.

In this article, we examine the selling pressure SaaS companies have faced in recent months and the underlying drivers of investor concern.

Indiscriminate selling

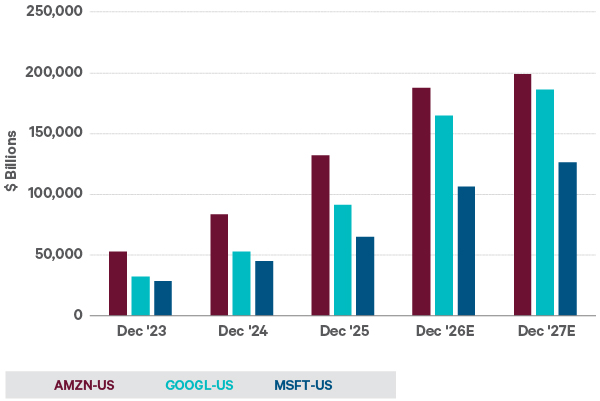

In January this year, Anthropic launched Claude Cowork, an important step in AI’s shift from chat-based assistants to more ‘agentic1’ systems that can carry out multi-step tasks. The release builds on a string of advances since ChatGPT brought generative AI into the mainstream in late 2022. Much of this rapid progress has been financed by mega-cap U.S. technology firms, which have poured capital into data centres and the chips needed to scale compute and power the world’s leading AI models. In 2026 alone, three of the so-called hyperscalers, Amazon, Google, and Microsoft, are forecast to spend close to US$500bn on AI infrastructure.

Figure 1: Google, Amazon and Microsoft’s technology capital expenditure

Source: Factset. Figures are in US dollars.

Claude Cowork represents the next link in the chain of development, not because it is ‘smarter’ in isolation, but because it changes the interface between AI and work. Investors have tracked developments closely, trying to assess which parts of the economy could be reshaped, and at what speed. In Cowork’s case, the introduction of domain-specific tools and plug-ins spanning areas such as legal work, finance, and customer support sharpened concerns that a broad set of SaaS vendors could be disintermediated, or at least see pricing power come under pressure. The result was a sharp, market-wide sell-off across software names, with the financial press, never short of a headline, quickly dubbing the episode the ‘SaaSpocalypse.’

Simple tools versus core systems

So far this year, the market has taken a ‘sell-first, investigate-later’ approach to anything with meaningful software exposure. In practice, that has meant a largely indiscriminate selling across a wide set of names, often without sufficient distinction between business models that are genuinely vulnerable and those that are structurally more resilient.

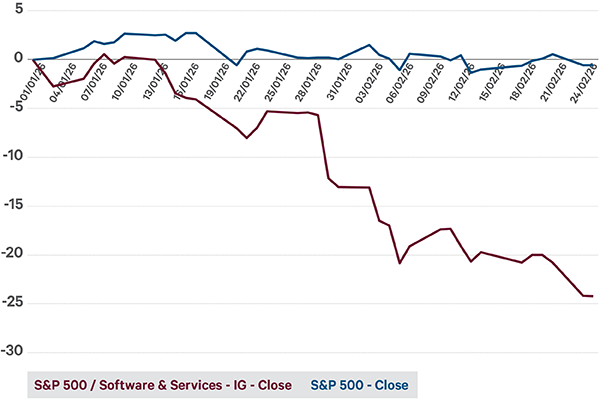

At this time of writing, the S&P 500 Software & Services subsector has underperformed the broader market by close to 20%. That blanket approach is unlikely to hold up, because ‘software’ is not one homogeneous category, exposure to AI disruption varies meaningfully depending on how embedded the product is, what data it controls, and whether it functions as a system of record or simply a convenient interface layer.

Figure 2: S&P 500 versus software and services

Source: Factset, February 24th 2026.

At their core, modern AI systems are powerful statistical engines. They learn patterns from large datasets and then generate outputs, predictions or actions, based on the information available to them. The practical implication is AI is only as useful as the quality of the data it can draw upon. The adage still applies, ‘garbage in, garbage out.’ If an AI system does not have access to critical business data, it likely will not perform effectively as a digital employee for that firm.

In an enterprise setting, that puts a premium on software vendors that sit closest to authoritative data, maintain governance and audit trails, and are deeply integrated into mission-critical workflows. One must also distinguish between probabilistic deterministic tasks2, the latter of which requires 100% accuracy all times. The risk of AI models ‘hallucinating’ or simply making up information, limits their efficacy as a solution for tasks which simply cannot bear risk of error.

From the customer’s perspective, some degree of AI-driven disruption is arguably a net positive. Enterprises have become bloated with overlapping tools, fragmented workflows, and multiple solutions that perform narrow functions. BetterCloud has estimated the average enterprise uses over 100 SaaS applications, a figure that accelerated sharply around the pandemic as teams adopted software quickly to stay productive. AI can act as a catalyst for that consolidation by reducing the need for standalone software apps.

However, rationalisation does not mean enterprises will rip out legacy systems altogether. A more likely outcome is a bifurcation2. On one side sit mission-critical platforms that are deeply embedded, data-rich, and central to governance, harder to replace and more likely to absorb AI as an enhancement rather than be displaced by it. That stickiness is even greater in regulated industries.

Banking is a good example. The question is not simply whether an AI tool can replicate existing functionality in theory; it is whether the organisation can migrate core customer records and operational processes to a new system with near-zero tolerance for error. The regulatory and operational consequences of a misstep, alongside the risk of reputational damage, create powerful incentives to move cautiously, reinforcing the status quo.

The flip side of that are more discretionary applications, often departmental, lightly integrated, where AI can replicate enough functionality to pressure pricing, reduce seat counts, or encourage consolidation. Should these software vendors fail to justify their value to the enterprise in the face of AI alternatives, they may indeed face extinction.

What are incumbents doing?

For software companies deeply embedded in enterprise workflows, where mission-critical data lives inside their systems, AI is a significant opportunity. Leaders like SAP and Salesforce are integrating cloud-based AI capabilities directly into their core platforms. On a recent investor call, SAP CEO Christian Klein highlighted strong early traction, noting that 90% of the company’s largest quarter four deals included an AI purchase. He emphasized that customers can’t simply pick a model from providers like OpenAI and expect it to run effectively on top of their business processes. Without access to essential enterprise data, such as the data housed within SAP, AI agents lack the context needed to deliver accurate, reliable results.

However, even the leading players do face challenges such as adapting their pricing models. If enterprises don’t replace incumbent vendors but instead deepen adoption through AI-enhanced versions of existing software, the question for software vendors becomes can they sustain historical growth and margins. Traditional SaaS economics were built on seat-based pricing: as companies hired more employees, they bought more user seats for tools like ERP. But if AI materially boosts productivity and introduces fleets of AI agents that function like digital employees, seat growth is likely to slow, stagnate, or even decline versus historical trends.

Several alternative pricing models are emerging. One is outcome-based pricing, where vendors charge based on the volume of work an AI agent completes in a certain period. Another potential option is consumption-based pricing, tied to usage metrics such as the amount of data processed.

More broadly, change is a constant feature in software and technology. The industry has already navigated major shifts, from one-time perpetual licenses with maintenance contracts to cloud-delivered, seat-based subscriptions. That cloud transition may offer a useful template for today’s moment: companies that fail to adapt may fall behind and even fail. While those that innovate can emerge stronger as AI materially enhances the value they deliver to customers.

Digital employees

The sell-off in software has coincided with a broader, and increasingly consequential, debate about the future of white-collar work. As AI systems move beyond answering questions toward executing tasks, investors and corporate leaders are reassessing which parts of the knowledge economy are most exposed, and how quickly adoption could translate into changes in headcount, hiring patterns, and productivity expectations.

Anthropic CEO Dario Amodei, has been among the most outspoken on this topic, warning that a substantial share of entry-level white-collar roles could be displaced within a relatively short time horizon. This concern is particularly acute in sectors such as legal services, where early-career professionals have traditionally developed expertise through high-volume, repeatable work including document review, basic contract analysis, and research summaries. These tasks are often rules-based and text-heavy, making them well-suited to the kinds of AI workflows that more easily automate.

Amodei’s warnings are not without substance as early signals already appear. In 2025, data from the consultancy Challenger, Gray & Christmas suggested that AI was increasingly being cited as a contributing factor in layoff decisions in the U.S., pointing to a shift in how companies frame efficiency programmes and workforce planning. In 2025 employers reported 55,000 layoffs were directly attributable to AI.

The implication is not simply that ‘jobs disappear,’ but that the structure of work may compress from the bottom. If routine work is increasingly automated, firms may need fewer juniors to produce the same output, and the classic apprenticeship model, where junior analysts and associates are trained through repetition, becomes harder to sustain. However, it should be noted past technology waves didn’t eliminate work so much as reallocate it, phasing out certain job types while spawning new functions and industries. If history is any guide, the advent of AI will likely lead to new types of jobs which are not in existence today.

Davy positioning

For investors, the key takeaway is that ‘software’ is not one trade. AI is likely to create winners and losers, and the recent sell-off has been a reminder of how quickly sentiment can shift when business models are questioned. In our equity portfolios, we hold exposure to quality software names such as SAP and Microsoft. Our software exposure is part of a broad diversified framework, with stock exposure spread across different industrial sectors and across regions.

Our approach is to concentrate on high-quality companies, typically those with strong competitive moats, recurring revenue characteristics, and the operational discipline to evolve their products and pricing as the industry changes. We believe the combination of diversification and a focus on quality, offers the best way to participate in the long-run opportunity while managing the near-term volatility that comes with a rapidly shifting technology landscape.

1 Agentic refers to having the capacity to act independently, make choices, and take purposeful action rather than being passive or controlled by external forces.

2 Deterministic tasks have fixed, predictable outcomes, while probabilistic tasks involve uncertainty and rely on likelihoods rather than guaranteed results.

3Bifurcation refers to a split into two distinct parts, paths, or outcomes.