In a surprising move, the UK is heading to the polls for a general election, earlier than expected, on 4th July. In this article, we consider the economic and political implications that investors should be considering.

Economic growth and inflation

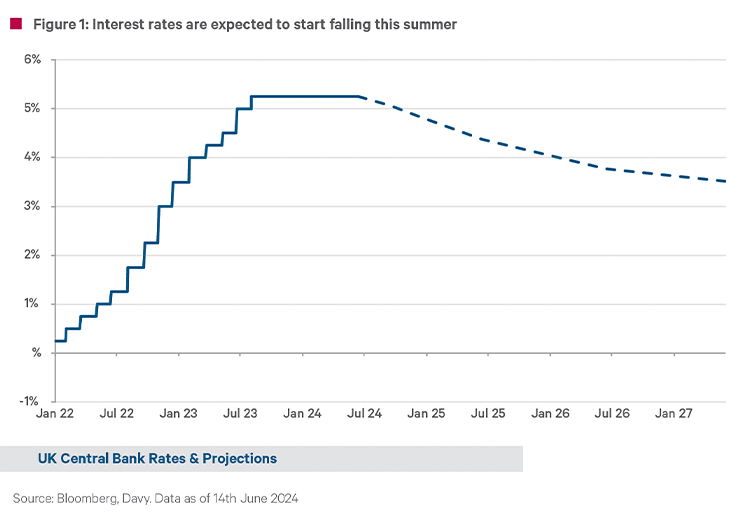

The UK posted a surprisingly robust first quarter GDP1, thus exiting its recessionary period. This was driven by temporary growth factors, which are unlikely to be repeated, therefore growth is expected to temper going forward. Real GDP growth for 2024 is forecast to be 0.6% (1.2% in 2025), which although low, remains positive. Headline inflation in the UK is at an elevated 2.3% but has been improving closer to the 2% target of the Bank of England (BoE). However, the easy lifting is done and was driven mostly by falling domestic energy bills. Therefore, the timing of the election does not fit well with the incumbent governments’ claim that inflation is under control, and growth is improving. In fact, the stubbornness of elevated inflation levels has delayed the timing and the magnitude of interest rate cuts, that the BoE would have forecast six months ago.

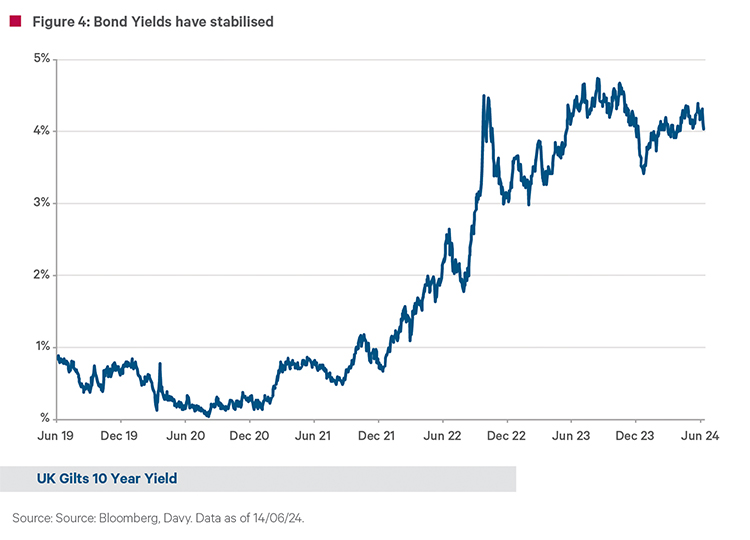

Interest rate cuts would be a very welcome relief for a heavily indebted UK mortgage market, which has seen interest rates rise faster than at any time in history. The BoE may become more tolerant of a ‘slightly’ elevated inflation outlook, which would be the price payable to sustaining an upward growth path. In this regard, we believe that the BoE will start cutting rates later this year, which will come too late for the incumbent government, and it is more likely to boost growth and support for the new government when they arrive.

Who will win?

The opinion polls are indicating that a surprise is not on the cards. The incumbent government trails heavily and would require a herculean turnaround in fortunes to win. The UK uses a ‘first past the post’ electoral system, so the one candidate with the most votes wins. In this binary ‘winner takes it all’ format, it is increasingly likely that the prospective new government will have a significant mandate.

This leaves market participants and investors pondering what the new government will deliver. The Labour party in the UK has not been part of a government since 2010. The personalities and policies have changed significantly in that time, meaning its policy intentions and the degree of socialist agenda will receive the greatest critique.

Policy review

There has been a distinct focus on ‘stability’ from the Labour campaign thus far, which is perhaps its easiest blow to land on the incumbent government. Labour has announced its intention to legislate for the mandatory provision of a forecast by the independent Office for Budgetary Responsibility (OBR). The UK’s 2022 mini budget did not provide the OBR with sufficient time to provide a fiscal assessment of the significant and permanent tax and spending changes. Markets see this as a strong stabilising move, given the previous incumbent government’s experience.

In addition, the rhetoric surrounding Labour’s relationship with business has changed markedly. Previously Labour held much less business friendly views, which has been a significant problem for the public since they left government in 2010. Labour has therefore been looking to enhance its reputation in financial markets and have a more business-friendly approach.

Concerns surrounding tax policy will continue to be Labour’s primary focus point, to make business and the public more comfortable. Public services and investment will remain a top focus for critics, but a selling point to the public for Labour. In terms of paying for this, they are looking to improve transparency and take a structured and differentiated fiscal policy; the current budget will look to be balanced using tax revenues (day to day running of public services), and any additional borrowing to be earmarked to pay for increased public investment. The intention is to offer debt investors’ confidence and transparency in the use of proceeds, enabling society to take advantage of long-term investment, reduce the overall debt burden over the medium term, and thus enhance debt sustainability.

A stable and structured approach is welcome, but tax increases are inevitable and will be necessary, no matter who forms the next government. This is despite the nation’s tax burden being at its highest levels since 1948.

It is worth noting that prior to the 1997 Labour electoral landside, the BoE independence was not debated on the campaign trail. It was one of Labour’s first major policy moves. Those lamenting a closer trading relationship with the European Union may see a thawing, and a large-majority Labour government may feel the timing is right to legislate for this. A singular EU/UK deal, which exhibits many of the Customs Union attributes, would come as a surprise for markets. This could be a catalyst for a boost to economic growth for both the UK and the European Union.

Investment outlook

Stability and the fiscal prudence may all seem short-term in nature, and they pale in comparison to the longer-term structural challenges facing the UK economy. However, the UK is not alone in that regard, with challenges surrounding an aging population, lack of productivity growth, the climate crisis, and more isolationist global trade relations.

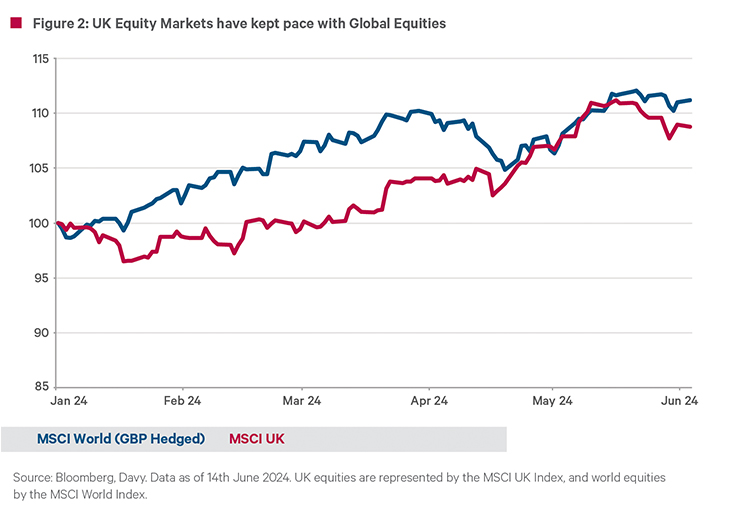

UK equities have underperformed the rest of the world in the rally year to date. MSCI UK index is up 7.6% year to date, and the MSCI World Index, 13.0% (both in GBP terms). However, the UK remains relatively attractive a valuation basis, trading on a price to earnings multiple of only 11.7 times versus global equities at 20.5 times. The cheaper multiple offers plenty of upside, should the opportunity arise.

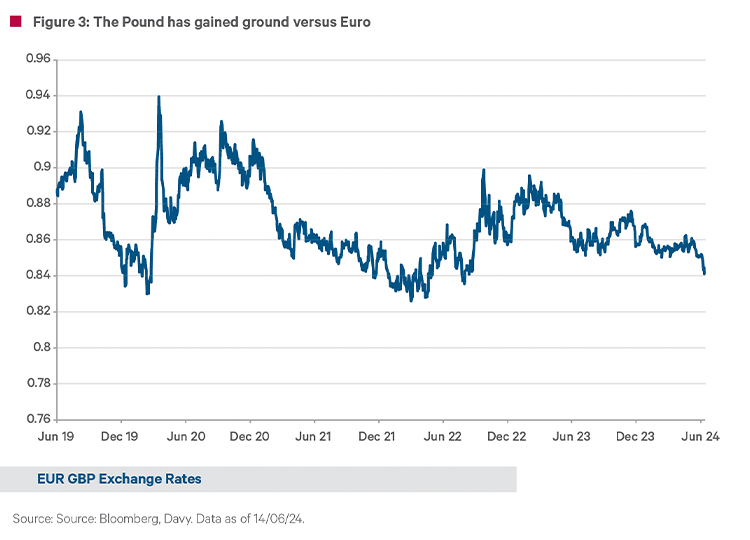

Markets have been pricing in a volatility ‘bump’ around the election date to allow for any UK-style surprises. A cautionary note was raised, after the Euro experienced some weakness versus Sterling following the results of European elections, specifically when French President Emanual Macron called a snap election after the far-right defeated his centrist alliance. Labour is expected to return to power for the first time in fourteen years. It remains to be seen if a change in the UK government will result in a significant shift in the relations between the UK and the European Union. A meaningful improvement in the relationship would likely provide an opportunity for the UK economy, Sterling, and broader financial markets.

The song by D:Ream, ‘Things can only get better’, became the election anthem for the Labour landslide return to government in 1997. Events in the last decade, have seen confidence and sentiment towards the UK fall to new lows. Opportunities are starting to emerge, and investors might be forgiven for beginning to feel that things can only get better.

1 GDP is Gross Domestic Product, the standard measure of economic growth.

If you would like to discuss anything covered in this article, please contact your Davy advisor.