Money market funds have been around for over half a century, yet they’ve never caught the imagination of Irish investors who were content to earn interest income on their cash through a bank deposit. In inflationary times, doing nothing could be your riskiest move. We offer a broad range of investment and liquidity solutions.

What is a money market fund?

A money market fund is a fund that invests in very short-term, high-quality debt issued by governments, financial institutions, and highly rated corporates. These characteristics make money market funds a low-risk investment option to invest surplus cash for the short term. Money market funds are primarily used to preserve capital, with a high degree of liquidity, and aim to generate a return in line with Central Bank deposit rates. They are daily liquid, meaning that your capital is not locked up.

Is cash really king?

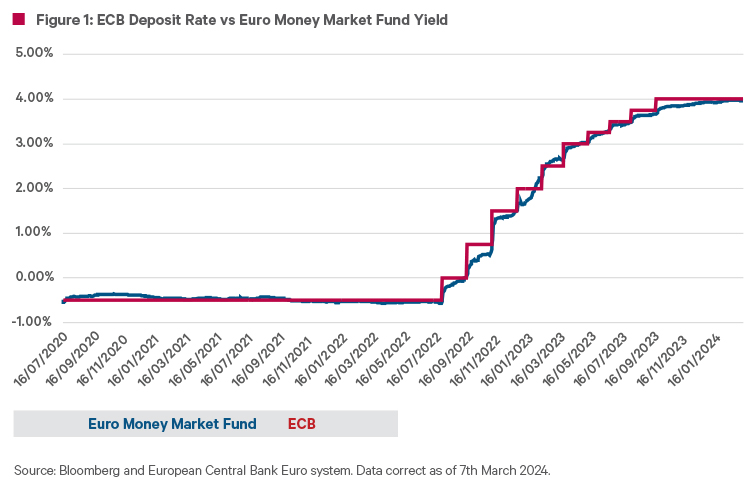

Although not quite as safe as cash, money market funds are considered very low on the risk spectrum. Money market funds invest in a highly diversified range of securities, issuers, and maturity profiles, whilst maintaining very high credit quality. Money market funds are particularly attractive when interest rates are rising. In a rising rate environment, as the short-term securities mature, they are reinvested at the higher prevailing rates. This means that increases in the Central Bank policy rates are passed on more quickly to investors in money market funds than they otherwise would be holding cash deposits in a bank. Thus, broadly speaking, the yield on money market funds should track the Central Bank base rates, albeit with a slight lag.

Bank deposits, on the other hand, are cash deposits with a single counterparty. The deposit rate is entirely dictated by the individual bank and the yield is influenced by the banks’ funding needs and balance sheet. As we have seen in recent months, the rates offered by many Irish banks have not yet risen in line with European Central Bank policy rates. For this reason, investors who are looking to capitalise on the increases in Central Bank interest rates could consider money market funds as a means to invest their cash over the short term.

What are the risks?

Money market funds, like most investments, are not risk-free. They may expose an investor to counterparty risk, liquidity risk, and credit risk, to name a few. The diversification benefits of money market funds enable the investor to mitigate many of these inherent investment and market risks. Money market funds can spread counterparty risk across many underlying issuers, which reduces the risk of capital loss. Bank deposits, on the other hand, expose the investor to a single counterparty. The events of 2008, while unlikely to happen again, highlight the importance of diversification and the risks of concentration of deposits with a single institution.

The credit ratings of money market funds are typically very high and range between AA to AAA rated on average. This means that the creditworthiness of the underlying government or corporate debt securities is of very high quality. To many investors’ surprise, the credit rating of a typical Irish bank, where many of us hold our cash deposits, is BBB-rated on average. Money market funds are arguably of higher credit quality than bank deposits.

Can money market funds lose money?

Given the short-term, high-quality nature of the underlying securities, money market funds are considered very low risk. But the risk of loss is not zero. The value of these securities can change day to day. As seen in the past, in the event of a highly stressed scenario, there is a small chance that the underlying assets can default. However, money market funds have become increasingly regulated over the past fifteen years which has led to greater confidence and stability in the asset class. For example, at the height of the COVID-19 crisis in March 2020, the worst-performing UK money market fund lost just -0.2% before recovering, according to Charles Stanley, December 2022.

The evolving regulatory landscape

Since the volatility caused by the Global Financial Crisis (GFC) in 2008, global financial regulators have since strengthened the rules and guidelines surrounding money market funds. The enhanced guidelines now require higher levels of diversification within the fund and require increased levels of liquidity. Further regulation in the asset class has raised standards in money market fund investing and ultimately aims to reduce the risk of capital loss. This makes, what is considered to be a safe asset class, even safer.

It no longer makes sense to keep your money under your mattress

Post the GFC in 2008, Central Banks reduced interest rates to record lows and they even dropped to negative in the Eurozone. Interest rates remained close to zero for almost a decade and the hunt for yield became practically impossible in short-term, high-quality debt. As a result, money market funds became irrelevant to investors searching for positive yield.

With inflation in the Eurozone reaching levels that we have not seen in decades, the old practice of keeping your money under your mattress no longer makes sense. The real, or inflation-adjustedvalue of your cash is being quickly eroded by the power of inflation. Money market funds may be one tool that investors consider if they have surplus cash to invest, to take advantage of higher Central Bank interest rates. The European Central Bank base rate now stands at 4% and the yield on Euro money market funds is now at, or outpacing this return. Although money market funds won’t outpace the rate of inflation in the long term, the short-term benefits of money market funds are clear. In the search for yield over the past decade, investors had to extend their risk appetite beyond what they would normally be comfortable with. There’s no need to reach for yield anymore. Relatively attractive yields on low-risk assets are back.