Book a consultation

We're ready to help you along your journey

0 topics selected

27 August, 2024

Beyond words goes here

The last few years have certainly thrown some curveballs. The importance of preparing for the unexpected has never been more relevant. However, many people continue to take a completely passive approach to something as significant as saving for retirement. Many are simply content to let their pension pot tick along in the background, under the assumption that all is well, the fund is growing and there’s nothing much to do except leave it alone and wait.

The idea of engaging with any major financial planning or decision making can seem daunting. It’s far easier to put it off, deal with it some other time. And besides, what’s to deal with? Isn’t it taking care of itself?

Your pension may indeed be ticking along, but it’s far too important to leave to its own devices. We’re all living longer and fuller lives and retirement doesn’t mean what it used to – for some it’s kicking back and taking some well-deserved time out, whereas for others it can be the beginning of new ventures. Whatever it means for you, with a little extra effort and attention now, you could realise significant gains in growing your nest egg.

While there is no one-size-fits-all, there are simple steps and easy fixes which can help ensure your fund is in peak condition.

For almost every client we work with, whether you’re in a company pension scheme, self-employed or a professional, experience has shown that the secret to a fulfilling retirement and delivering the best outcomes for clients is planning. Not necessarily saving, or sacrificing, or working harder – although of course, they come into it too – but thinking and planning ahead.

Some of the things I ask every client up front is ‘How financially secure do you want to be when you retire? What’s your retirement number, i.e. What level of assets do you need to accumulate over your working life to secure the level of retirement you want?’

This hypothetical figure is the starting point for nearly every conversation about retirement. It focuses the mind. Get that number down on paper first, and work from there.

Making regular contributions to your pension fund is the bare minimum – but on its own, it’s not enough. You also need to invest your fund so that it generates the return you need on your investment.

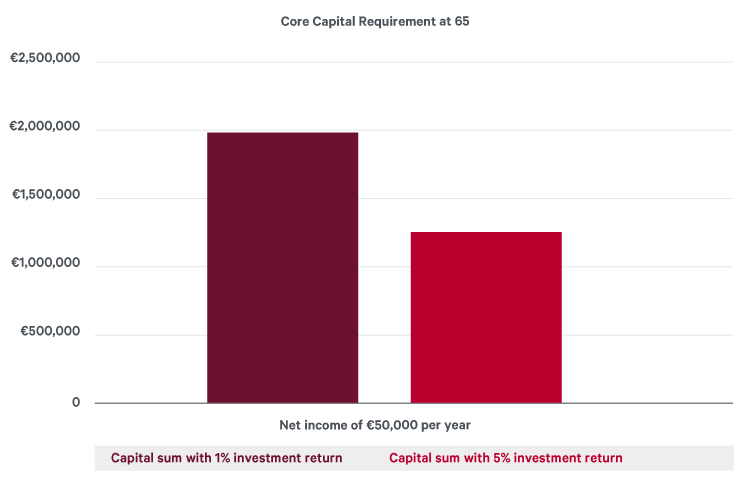

Figure 1 below illustrates a core capital requirement to provide a net income of €50,000 per annum, inflation adjusted annually at 2%, from age 65 using two different investment approaches.

Source: Davy October 2021. The figures in the chart are for illustrative purposes only.

A defensive approach to investing in cash and bonds may return 1% over the long term (and less in the short term in periods of negative interest rates). Following this investment approach, you would need €2m in core capital at age 65, in comparison to €1.3m of core capital required if you were to invest in a long-term portfolio, as investment growth will do a lot of the hard work for you. This may be a more volatile portfolio but you will likely have time on your side to ride any storms that the markets may bring.

Having a financial plan in place will ensure that your pension and investment approach is tailored to your personal circumstances and built around, amongst other things, your specific retirement plan.

Investing in a pension over the long term and contributing to it regularly undoubtably is the most tax efficient way to build up a nest egg towards your core capital retirement pot. Not only do you get income tax relief on your contributions, but the income and gains within the pension fund can roll up free of income tax, CGT (capital gains tax) and fund exit tax.

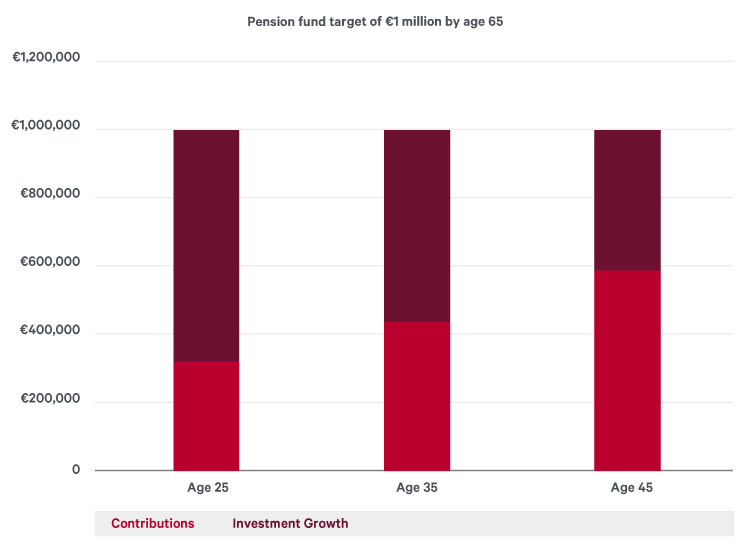

And as the following example illustrates, the sooner you start, the better the outcome.

In our example in Figure 2 we have three individuals who are targeting a pension fund of €1m at age 651. Our early-starting 25-year-old needs to contribute just €7,820p.a. whereas our further-down-the-track 45-year-old has to contribute circa. €28,000p.a. to achieve the same result. The contributions made over the working life of the 25- year-old are significantly lower as there is much more time for tax-free investment growth to do the hard work. It results in a pretty remarkable difference in contributions.

1Assumes 5% growth, not inflation adjusted

Source: Davy October 2021. The figures in the chart are for illustrative purposes only.

Another one of those ‘rough’ ideas that could be impacting your pension plan. You may be entitled to tax relief on pension contributions but do you know how much it’s worth to you?

If you are higher rate taxpayer, then subject to certain criteria and limits, for every €1 you contribute to a pension, the exchequer will give you back approximately €0.40. Even if you have never been self-employed or never had to file a tax return, you may have scope to make pension contributions that qualify for tax relief for 2020*.

Some employers will offer a company scheme that matches or even doubles employees’ contributions. Your €1 contribution can translate into a €3 injection to your pension when you take account of your own contribution plus a € 2 employer contribution. This is an obvious benefit to take advantage of €2 employer contribution.

*www.revenue.ie/en/jobs-and-pensions/pensions/tax-relief-for-pension-contributions.aspx

Many of us have different pensions invested in different places. Not understanding, or worse, not paying attention to fees and charges, can have a significant impact on the future value of your pension pot(s). Most pension arrangements charge an annual management fee but it is vital that you also understand the costs associated with the specific fund(s) you choose. For example, commission, fund manager charges, bid/offer spreads and custody fees.

Your pension provider or adviser can provide you with a detailed breakdown of all costs associated with the operation and investment management of your investments – all you have to do is ask.

We’re all unique in terms of our circumstances, our resources, and we all differ when it comes to how much we need to set aside to have a comfortable retirement.

However, too often, a one size fits all investment approach is applied to pension savers. Even lifestyle funds, which aim to de-risk pension members as they approach retirement, can be far too generic. They make a general assumption that we all want the same things when we retire.

A more personalised approach can help you get to where to want to be with the level of risk that you are comfortable taking will ensure continuity of advice on an ongoing basis into retirement and beyond. So what’s the solution? Get the best advice of your life, for your life.

If any – or all – of this rings true, it’s probably time for a thorough review of your retirement funding strategy. Getting expert advice is a good place to start.

At Davy, we understand that our clients are individuals, each with different financial goals. We don’t do ‘one-size-fits- all’ pension plans because how much you need in retirement differs for everyone. Your retirement number is entirely personal to you. That's why we match you with specialist advisers who spend time getting a genuine understanding of your life and finding out what matters to you, so that we can deliver the results you’re looking for.

Warning: The value of your investment may go down as well as up.

Detailed criteria must be satisfied in order for a pension contribution to qualify for tax relief. The tax information contained in this article is based on Davy’s current understanding of the tax legislation in Ireland and the Revenue interpretation thereof. It is provided by way of general guidance only and is neither exhaustive nor definitive and is subject to change without notice. It is not a substitute for professional advice. You should consult your tax adviser about the rules that apply in your individual circumstances. Davy is not responsible for the interpretation of this information and any submissions made by you or a third party on your behalf thereon.

It all begins with a simple, no obligation conversation.

For investors who are comfortable making their own investment decisions.