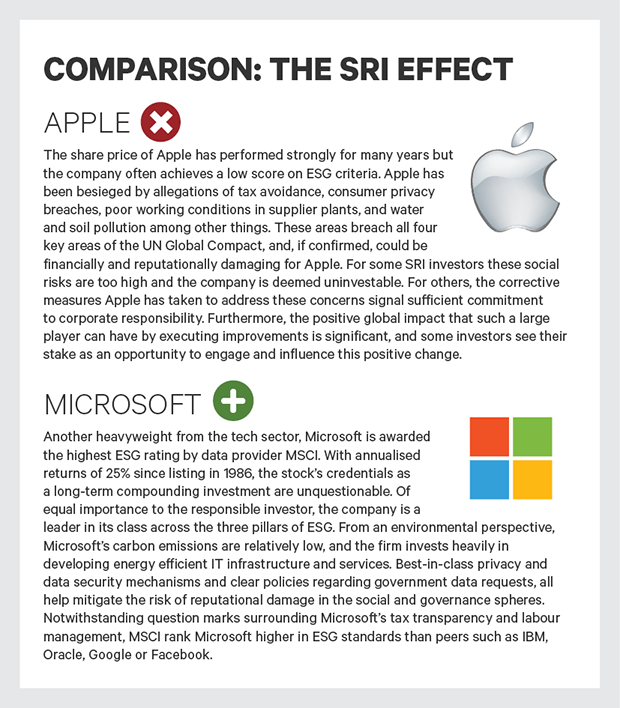

MarketWatch - Socially Responsible Investing

This article is from our latest edition of MarketWatch, an in-depth report focusing on Socially Responsible Investing.

Patrick McLaughlin ESG Multi-Asset Portfolio Manager

02nd May, 2018

Changing societal norms has led to a massive increase in the amount of money invested in socially responsible investing (SRI) strategies. The growing focus among world leaders on climate change, the heightened corporate regulation following the global financial crisis, and increasing concerns over data protection and security breaches represent issues not typically addressed by traditional investment analysis.

SRI is not a new phenomenon. As far back as 1758, the Religious Society of Friends (Quakers) outlawed its members from investing in the slave trade and since then investors have been applying similar values to their investment principles. Ethical investing, which today comes under the many guises of SRI investing, gained significant traction in the latter part of the 20th century. It was largely driven by the demands of large university endowments and faith-based institutions looking to avoid investing in companies with exposure to controversial industries – the so-called “sin stocks”.

Although ethical investing's roots are firmly founded in the strategies favoured by charities and religious congregations, today SRI is not simply about excluding controversial industries like alcohol, tobacco, weapons or gambling, but now extends to identifying good corporate, environmental and social practices amongst other areas. More recently some high profile catastrophes have helped to increase the focus on responsible investing. Nuclear disasters (Fukushima), collapsing factories (Dhaka), oil spills (Exxon Valdez) and vehicle emission scandals (Volkswagen) have all proven detrimental to the environment, to society and to any investor who happened to hold the stock through the affected period.

![]()

Source: CFA Institute, environmental, social, and governance issues in investing (2015)

SRI investors typically evaluate companies under the 3-pronged environmental, social and governance (ESG) approach. Table 1 outlines examples of the business factors that might be considered.

These criteria can have a significant impact on economic performance. For example, high carbon emissions or poor waste management may result in costly fines, while weak labour standards and poor employee engagement will likely result in expenses from staff turnover.

On the flipside, companies that invest in energy efficiency will reduce long-term costs and investing in staff training can drive innovation and competitive advantage. At the governance level, history has taught us that board composition and accounting practices are huge factors in corporate bankruptcies. Taking stock of these factors may help us avoid scenarios such as the collapse of Enron or Anglo Irish Bank.

The evolution of SRI has spawned an array of new disciplines and an accompanying selection of phrases to describe them. The boundaries are blurred between these disciplines and are not universally agreed. Responsible investing can mean different things to different investors. Terms such as ethical investing, impact investing, ESG or SRI are often used interchangeably. However, we believe that subtle differences exist across this spectrum. Table 2 outlines some of the most recognised terminology and outlines our interpretation of the differences between each.

![]()

Source: A Preliminary Report on The Sources of Ireland’s Banking Crisis, Klaus Regling and Max Watson

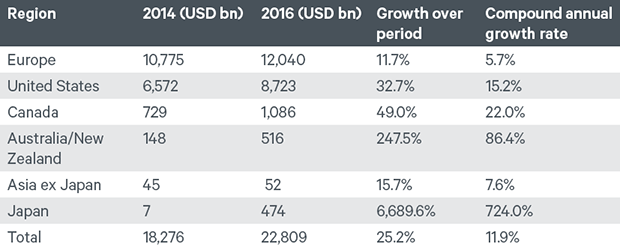

The impressive performance of responsible investments has been one of the key factors in its recent growth. The most recent figures estimate the total value of investments managed responsibly to be in the region of US$23 trillion. Between 2014 and 2016, global SRI assets increased over 25% and now account for approximately a quarter of all assets managed globally. Europe has been at the forefront of this trend and accounts for over 50% of the world’s SRI, while the US is the second largest with a 38% share. In Europe and Australia/New Zealand more assets are now managed in SRI strategies than non-SRI.

Source: Global Sustainable Investment Alliance Asia ex Japan 2014 assets are represented in US dollars based on the exchange rates at year-end 2013. All other 2014 assets, as well as all 2016 assets, are converted to US dollars based on exchange rates at year-end 2015.

SRI’s popularity is growing across all major demographics. Existing investments and interest levels are higher for women than men and are greater for millennials compared to other generations. However, the trajectory is positive across all sectors as more investors appreciate the benefits of an SRI approach and growth in these assets looks set to continue.

Ongoing FDA (Food and Drug Administration) investigations into tobacco companies and a continued distaste for guns, following mass shootings in the US, have also highlighted the benefits of a responsible approach. By avoiding the negative market reaction to these high profile events and focusing on strong ESG ratings, socially responsible indices have outperformed their unscreened counterparts.

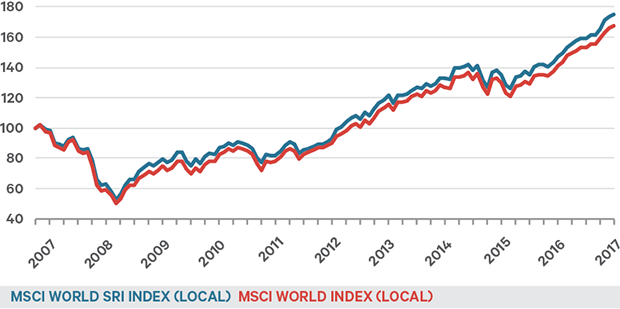

While ESG issues are usually straightforward to measure (e.g. the employee turnover for a company or the number of independent directors on a board), it can be more difficult to estimate their potential monetary value. The aggregate effect, however, can be observed by comparing the performance of two indices: one tilted towards good ESG companies, the other unscreened.

Source: Bloomberg

SRI analysis and the ESG attributes outlined all facilitate the selection of better quality investments. Over the long term, this translates into better investment returns. Since its inception in 2007, the MSCI World SRI Index has outperformed its non-SRI counterpart by 7.6%, or 0.7% annualised.

Interestingly the SRI effect is most pronounced in less developed markets, where the divide between good and bad ESG companies is greater. The MSCI Emerging Markets SRI Index has outperformed its non-SRI parent index by over 23% since inception, equivalent to 3.2% per annum. Moreover, the SRI index has achieved this outperformance with considerably less volatility.

The growing demand for responsible investments over the last number of years has forced companies and their management to address their exposure to ESG issues. The result of this benefits all of society: reduced carbon emissions and better waste management mean less pollution and a healthier environment; better labour standards and awareness of human rights benefit employees, customers and the supply chain alike; and improved controls at a governance level help instil confidence in management and avoid the costs associated with corruption and litigation. As we have seen, this translates into better investment performance over the long term.

The self-perpetuating nature of this relationship has already caused SRI to surpass non-SRI assets in many countries, and other regions and demographics look set to follow suit. With an outcome that provides societal benefits as well as strong investment returns, it is difficult to conceive what might derail the growth in SRI.

This article is from our latest edition of MarketWatch, an in-depth report focusing on Socially Responsible Investing.

Warning: Past performance is not a reliable guide to future performance. The value of investments and of any income derived from them may go down as well as up. You may not get back all of your original investment. Returns on investments may increase or decrease as a result of currency fluctuations.

Warning: Forecasts are not a reliable indicator of future performance.

Patrick McLaughlin ESG Multi-Asset Portfolio Manager

This article is from our latest edition of MarketWatch, an in-depth report focusing on Socially Responsible Investing.