MarketWatch - Socially Responsible Investing

This article is from our latest edition of MarketWatch, an in-depth report focusing on Socially Responsible Investing.

Conall MacCoille Chief Economist

02nd May, 2018

There is no doubt that the Irish economy enjoyed strong growth last year. But the recent 7.8% gross domestic product (GDP) growth figure overstates the pace of the recovery - once again distorted by ‘leprechaun economics’ related to the multinational sector.

In 2017 employment expanded by 2.9%, tax revenues by 6% and retail sales (excluding motor trade) by 4%. These are exceptional rates of growth and suggest that Ireland is probably the fastest growing economy in Europe. However, there are some grey clouds on the horizon. Despite some progress on the Brexit negotiations, the thorny issue of the Northern Ireland border remains unresolved. So the possibility of failing to negotiate a new agreement by the March 2019 deadline cannot be ruled out. The silver lining is that a transitional arrangement until 2020 has been agreed and this should provide some certainty for business - not least small Irish companies exporting to the UK.

For now the multinational sector remains a key source of growth. Employment in multinational companies operating in Ireland increased 5.3% in 2017, to 210,000. However, the outlook for foreign direct investment (FDI) is uncertain given global tax reforms. But for now the impact of President Trump’s tax reforms seem manageable. EU Commission proposals for a common consolidated corporate tax base (CCCTB) and a 3% levy on digital companies, such as Google and Facebook, could be more damaging.

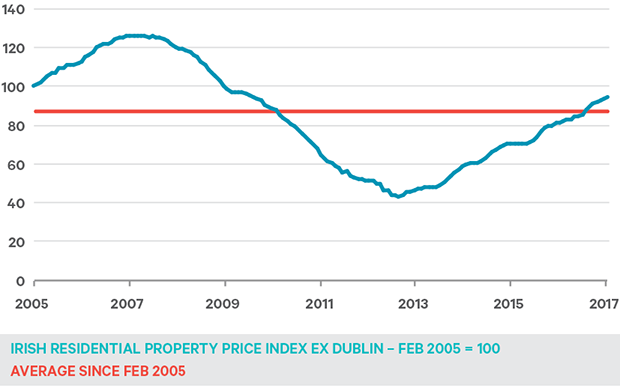

House prices continue to rise The housing market remains a thorn in the side of the Irish government. Double-digit house price inflation has continued into 2018, accelerating to 12.5% in January. As the pace of house price inflation has been so strong, the Central Bank has tightened its mortgage lending rules. Meanwhile, rents continue to rise. Rents increased 6.4% in 2017 and the average rent at the end of 2017 was €1,050 per month, and €1,500 in Dublin. In December 2017, Minister for Housing Eoghan Murphy announced new minimum standards for apartments in an attempt to boost supply by reducing construction costs. These included exemptions for car parking spaces in apartments close to city centers and public transport. Homebuilding levels are estimated at close to 12,000 units per annum, well below demand of at least 35,000. The risk is that this bottleneck will start to hold back economic growth – especially in the capital where the lack of residential property is most severe.

Source: Bloomberg

In February the government launched its National Development Plan which set out its spending priorities as capital expenditure is ramped up to €8 billion per annum by 2021. Headline grabbing projects included an airport rail link in Dublin, a Cork-Limerick motorway and an extension to the DART by 2027. The plan also intends to reduce the dominance of Dublin, by facilitating 50-60% growth in Cork, Galway, Limerick and Waterford. This will mean prioritising these areas for infrastructural investment over more rural locations. However, this may be difficult to deliver politically. So it remains to be seen whether Ireland’s ‘new politics’ can overcome the ‘one for everyone in the audience’ mentality.

This article is from our latest edition of MarketWatch, an in-depth report focusing on Socially Responsible Investing.

Conall MacCoille Chief Economist

This article is from our latest edition of MarketWatch, an in-depth report focusing on Socially Responsible Investing.